Saying Goodbye To The Kojo Nnamdi Show

On this last episode, we look back on 23 years of joyous, difficult and always informative conversation.

After last year’s rocky rollout of the Affordable Care Act’s signature marketplaces, including Healthcare.gov and Maryland’s health exchange, the pressure is on as this year’s open enrollment season launches. At the same time, political foes of Obamacare are ramping up challenges to the law. We explore what you need to know about health care exchanges.

“You’ll be okay. Probably.” In a new ad, Illinois adopts a cheeky approach to get millennials signed up for health insurance.

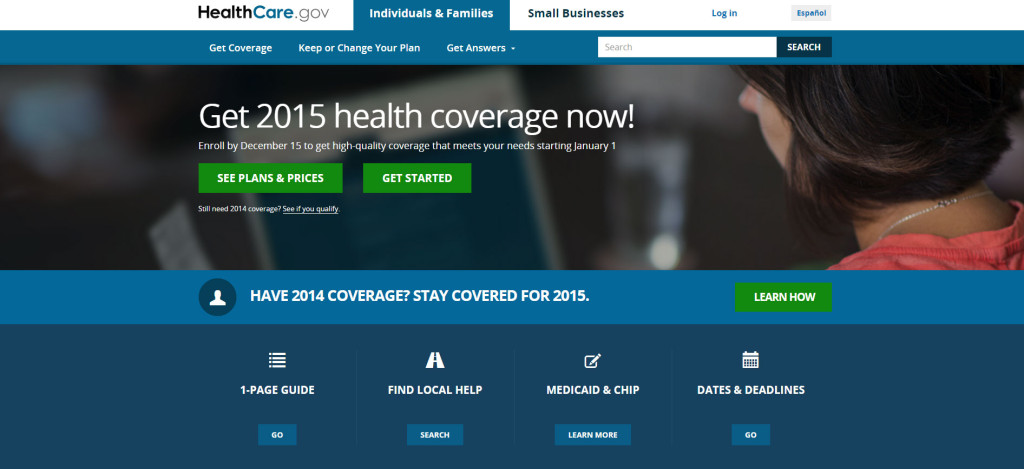

MR. KOJO NNAMDIFrom WAMU 88.5 at American University in Washington, welcome to "The Kojo Nnamdi Show," connecting your neighborhood with the world. Last year at this time, Obamacare signature marketplace for the Affordable Care Act, healthcare.gov, failed in dramatic fashion when it rolled out and some states didn't fare much better, including right here in our region where the Maryland Health Connection website crashed repeatedly.

MR. KOJO NNAMDIThe good news is that for this year's open enrollment season, which began on Saturday, technical issues seem to have been addresses, allowing those looking for health care coverage to focus on the bigger questions around plan choices. Joining us to discuss all of this is Alice Weiss. She is the program director for the National Academy for State Health Policy or NASHP, an independent organization of state health policymakers. Alice Weiss, thank you for joining us.

MS. ALICE WEISSGlad to be here, Kojo.

NNAMDIAlso with us in studio is Jenna Johnson. She is a reporter with the Washington Post. Jenna, thank you for joining us.

MS. JENNA JOHNSONThanks for having me.

NNAMDIJoining us by phone is Kimberly Lankford, contributing editor with Kiplinger's Personal Finance. Kim, thank you for joining us.

MS. KIMBERLY LANKFORDOh, it's my pleasure. Thanks for having me.

NNAMDIYou too can join the conversation. If you have questions, give us a call at 800-433-8850. You can send email to kojo@wamu.org or shoot us a tweet @kojoshow. Did you enroll in health coverage through a government marketplace last year? What was your experience? 800-433-8850. Kim, I'll start with you. In the midst of the open enrollment period for health care exchanges, let's start with the basics. What are the dates for singing up?

LANKFORDWell, open enrollment started November 15th and it lasts until February 15th. But there's a key deadline before then. If you want your new coverage to start by January 1st, you need to enroll by December 15th. So that really doesn't give you a lot of time to pick a plan. Also another key thing is that if you already had a plan from last year that you bought on the exchanges, as long as it's still being offered again, and most of them are, you will be able to automatically enroll in that plan again for next year.

LANKFORDBut it's a really good idea to go to your state marketplace and find out what all your options are because there's a lot of new options now. Some of the plans have changed their pricing, some have changed their networks. And in some areas, there's more insurers than there have in the past. So you may have many more options than you did last year.

NNAMDIWe are going to get into all of that during the course of this discussion. But, Alice, the different kinds of marketplaces are somewhat confusing, even to people who feel that we've been paying attention. Can you remind us of the various exchange options out there depending on your state and what they mean?

WEISSGreat. Sure, Kojo. So, there are basically three different varieties of exchanges or marketplaces that are available. The first is state-based exchanges. And those are state -- situations where the state is hosting its own insurance marketplace and you can go and buy coverage online from that entity. There are about 16 states, including D.C., that are offering state-based exchanges. The other variety are states that are working with the a federally facilitated marketplace, healthcare.gov to offer coverage.

WEISSAnd there are about 35 states that are doing that. Some states had the option in the first year of implementation to take a more active role. And those states were able to opt to either manage their insurance plans in the state or do more consumer-assistance work even though they were using the healthcare.gov options. And those are called federally facilitated partnership states. And there are about six states that are doing that option.

NNAMDIDid we mention state partnership marketplaces?

WEISSYes, yes. I call them federally facilitated partnership states, but you can...

NNAMDIWhat's the difference between that and a federally supported state-based marketplace?

WEISSAh, federally supported state-based marketplace. Well, there are state-based exchanges, marketplaces that are using the healthcare.gov platform because they had a little bit of trouble with implementing their own systems the first go-round. And they decided for the second year of open enrollment to be safe that they were going to rely on healthcare.gov to provide the technical platform even though the state is still technically running its own exchange. It's a little complicated.

NNAMDIIf you're confused yourself, give us a call. We can help. 800-433-8850. Kim, now someone in our area that might live in Virginia, D.C. or Maryland, and each of those is a different system, so how does that work? It's my understanding that healthcare.gov is a little like a front door. What then?

LANKFORDWell, that's true. You can go to healthcare.gov and input your zip code and it'll connect you to the marketplace in your area. And, for example, for Virginia, you will go through healthcare.gov. It's one of the federally run marketplaces. In D.C., it's DChealthlink.com and Maryland is Marylandhealthconnection.gov. And each of them has their own, you know, their own framework for doing things.

LANKFORDBut the key thing there is that you can get the prices for the policies and get policy details, which is really, really important to compare it easier. So, not only looking at the premiums, but also what your expected out-of-pocket costs to be for the types of medical care you usually have.

NNAMDIIn case you're just joining us, we are talking, in a way, about Obamacare round 2, the health care exchange's open enrollment period. If you have questions or comments, give us a call at 800-433-8850. You can email to kojo@wamu.org. You can go to our website, kojoshow.org, ask a question or make a comment there. Alice Weiss, one of the more important aspects is this early stage and screening people to see what sort of coverage they might qualify for. Can you explain?

WEISSRight. So everyone who applies for coverage through a marketplace option has to, first, be screened. If they want -- if they want help from the federal government to pay for their coverage, they have to first be screened and see if they're eligible for the public coverage programs, like Medicaid and the Children's Health Insurance Program that may be offered in the state. And if they're eligible for those programs, then they have to be enrolled into those programs as opposed to getting a tax credit, subsidy to support their coverage in the marketplace.

WEISSSo, every person who walks in that front door, whether it's a federally facilitated marketplace or a state-based marketplace, has to first go through that screening process if they want help.

NNAMDIJenna, Maryland did something of a soft launch. Can you talk about how Maryland did that over the weekend?

JOHNSONSure. Well, compared to last year, they wanted to give themselves a little bit more room to make sure that all technical bugs were worked out before masses of people started showing up. So, Saturday was opening day for all state exchanges and for the federal exchange. But in Maryland, if you wanted to sign up for health insurance, you actually had to go to Anne Arundel County and go to an enrollment fair at a middle school.

JOHNSONAnd about 200 people did that. On Sunday, a call center opened up. And if you called in, someone at the call center would help you get enrolled. The idea being let's only let a few people onto the system until we make sure that it's working. And then Monday, whether people knew it or not, it was open for business. And, you know, a few thousand people have already signed up for coverage. I keep logging on and putting in different combinations and it seems to be working so far.

NNAMDII tell you who heard about it, Steve in Columbia, MD. Steve, you're on the air, go ahead please.

STEVEWell, hello. Thank you for taking my call. I signed up for health care last year and it was a fiasco. I eventually got it. Took me a long time. This morning, I went to sign up for year two and it took about 30 to 40 minutes and it's done. So I had a much different experience and much better experience.

NNAMDIThank you very much for your call. It would appear that the soft rollout indeed worked, Jenna.

JOHNSONWe will see.

NNAMDIIn Steve's case certainly. Steve, thank you for your call. Alice, we all recall the disastrous rollout of the federal program, healthcare.gov, last year. Open enrollment began over the weekend. There's a lot of pressure for things to go right. Exchanges and their portals, websites seems to be -- seem to be in much better shape going into this enrollment season. What did healthcare.gov do to ensure that things would work this time around?

WEISSHealthcare.gov made a number of improvements. I mean, they spent a lot of time ensuring that their systems that were more functionally going to work together. So, basically, they created a new streamlined application that's going to make it easier for first time and release to go through the process more quickly. It has fewer screens. It's more dynamic. They insist that this is going to cut down on volume.

WEISSThey also, I believe, expanded their volume, so they could make it work. But I do want to stress that there's a lot of work that's happening that's not necessarily just healthcare.gov. Healthcare.gov is a really important front door, but there is so much work that has been happening in the states. States also have to have a front door for their Medicaid and Children's Health Insurance Program options.

WEISSAnd many states have been working to ensure that their systems are functional, that they can do the same types of online applications. They can interface with the federal government, identity verification systems and things like that. So there's -- there's a ton of work that's been going on in states that's valuable to (word?).

NNAMDICare to be any more specific about what some of the states did?

WEISSWell, I mean, Virginia was a state that definitely had a number of challenges last year. And I know that they've been putting a lot of work into their system to ensure that it can handle more volume and that things will be managed -- more centralized. There are a number of states that took these enrollment shortcuts that the federal government offered, where basically they were creating these options for people who they know, people who are already enrolled in public programs like nutrition assistance programs or SNAP.

WEISSThey would look at their eligibility information and basically borrow that information and determine them automatically eligible and enroll them into Medicaid coverage when they became eligible last year. And a couple of states like Arkansas and West Virginia ended up enrolling half of their expansion populations -- their Medicaid expansion population through this and it was quick, it was easy, it was cheap, and it helped keep that volume down so they didn't end up with a case backlog.

NNAMDIJenna, Maryland, of course, was one of those websites that crashed on day one last year. What did Maryland do to fix the issues with their system last year?

JOHNSONWell, they completely rebuilt the system. They took code from Connecticut. Connecticut's exchange was one of the most successful in the country. And so, Maryland was able to borrow that code and kind of customize it for themselves, switch out Connecticut for Maryland and put in their own information and things like that. And so, over the course of a few months, they very quickly rebuilt this site.

JOHNSONSo it's a brand new thing. Probably the feature that I hear the most about is that Marylanders can now go on and browse and shop without having to create an account, just like you would browse for an airline fare before you enter your credit card number. And they're hoping that that will get more people to be curious and to look and see if they can afford to have coverage this year.

NNAMDIOn to Robert in Boonsboro, MD. Robert, your turn.

ROBERTThank you, Kojo. Yeah, basically, I went through Maryland's exchange last year. I didn't have any real issues. It did take a little while, but it all seem to work out great. They sent my -- I got qualified for the Medicaid. They sent me my card. Now, this year, I was just wondering, I actually misplaced my card and I'm having some issues figuring out how to have them send me a new card.

ROBERTNow, I heard that I would automatically be renewed with the current coverage, which would be great. I was happy with it. But I don't have my card anymore. So I was wondering if there, you know, is there a good way to have them to send me a new card or if that's going to happen automatically when I get re-enrolled?

NNAMDIKim, can you answer that?

LANKFORDWell, of you were enrolled in Medicaid and if you still qualify for that, it's probably that, you know, you can go back to the marketplace and find the contact information, just see if they'll send you a new card. But you may want to go in and put all your income information in again just to make sure that you'll still qualify. And that's also a key thing for people not just people on Medicaid, but people who are receiving the subsidies.

LANKFORDIn most cases, if you still are -- if your policy still exists and they automatically reenroll you for next year, they will use the income levels that you had specified for last year. And if you had a big increase or decrease in income or if you have a life change, if you got married, divorced, it’s really important to go back into the marketplace and resubmit that information so your subsidy is accurate during the year.

LANKFORDBecause if you end up getting more subsidy than you should have, you'll end up having to pay that back at tax time next year. And if you don't get as much as you should have, you were missing out on that during the year. So, it wouldn't hurt to go back to the marketplace. But, you know, if you're really specifically looking for the card, just give them a call. All of the states have really beefed up their customer service lines this year. That was something that, you know, they realized they didn't have enough people working on last year. They also have a lot more in-person navigators. And also many of the states are working with agents, as well, to help people. So that's not as much a Medicaid issue, but really they have a lot more ways to get help, instead of just going through the website.

NNAMDIRobert, thank…

ROBERTOkay. Great.

NNAMDIRobert, thank you very much for your call.

ROBERTThank you.

NNAMDIJenna, Robert's call underscores another point. And that is the technology might not be the biggest challenge this year for Maryland, but getting Maryland residents to understand their coverage and what they need to do might be that challenge. What do people need to know in Maryland?

JOHNSONSo the big challenges this year are -- one is getting all the people who enrolled in subsidized care last year, to come back and reenroll. You must do that by December 18th. If you don't do that by December 18th, your coverage will continue, but your subsidy will not continue. So if you want to continue to have government subsidized health insurance you have to reapply through the new system.

JOHNSONAnd then the other challenge is Maryland didn't come close to enrolling as many people as they had hoped to enroll in private plans during the first enrollment period. And so they really need to get out there and get more people to sign up. Get more people to look at their options and see if they qualify for Medicaid, see if they qualify for a subsidized plan that can fit into their budget.

NNAMDIAlice, a lot of the work that Jenna's talking about involves educating the public as to all of these options. Can you talk about that?

WEISSSure. So there's a lot of work that needs to happen for people to understand, you know, even what their coverage options are, what the process is. And I think, you know, there's a lot of really great work that's happening right now, both at the federal level and the state level to help inform people about these topics, which are so complicated. A number of states have put together brochures to help people understand their coverage options.

WEISSMontana is a state that had an insurance website called Ask Away, where people could come in and type in a question because, you know, we know that this is a really complicated situation. So I think that there's a lot that states and the federal government are doing to try to sort of make it simpler. The federal government's putting out a lot of messaging around sort of, you know, get enrolled, you know, make sure you're -- make sure you stay enrolled.

WEISSAnd I think that message about, you know, that we're hearing about sort of making sure that you enter your new information in and not letting it renew automatically is really important, too.

NNAMDIOne of the challenges is getting young people to sign up. We'll talk about that later in the broadcast. Right now we've got to take a short break. But you can still call with your questions or comments, 800-433-8850. Are you considering going to a health care marketplace for health coverage? Are you part time or a freelancer who's considering signing up for health insurance through one of the health care marketplaces? Give us a call, 800-433-8850. Shoot us an email at kojo@wamu.org, a tweet @kojoshow or go to our website, kojoshow.org. I'm Kojo Nnamdi.

NNAMDIWelcome back. We're talking about Obamacare round two. It's open enrollment for the health care exchanges under the Affordable Care Act. We're talking with Alice Weiss, program director for the National Academy for State Health Policy or NASHP. It's an independent organization of state health policymakers. Jenna Johnson is a reporter with the Washington Post. And Kimberly Lankford is a contributing editor with Kiplinger's Personal Finance.

NNAMDIYou can call us at 800-433-8850. Alice, getting younger people to sign up is one of the bigger challenges. And education is a part of it. I'd like to play an ad from the campaign in Illinois.

ANNOUNCERNow there's a health plan for people who can't stand paperwork, a plan with no co-pays, a plan with no monthly premiums, a plan with no real health care of any kind. Introducing the luck health plan.

UNIDENTIFIED WOMAN #1No actual health coverage.

ANNOUNCERThere's literally nothing to it.

UNIDENTIFIED MAN #1That's what I call freedom.

ANNOUNCERIt's called the luck plan for a reason. It's based entirely on luck.

UNIDENTIFIED MAN #2I just cross my fingers and hope for the best.

ANNOUNCERThe luck health plan.

UNIDENTIFIED WOMAN #2You'll be okay probably.

NNAMDIHey, it's got the magic word, free, in it. But nevertheless, Alice Weiss, talk about the -- that group of potential enrollees, young people, and the special challenges there.

WEISSWell, I have to say first that I just love that ad. What you can't see on the radio is that the ad is filled with really attractive young people, but they all have these do-it-yourself splints, made of cardboard or bubble wrap. And it's just a hilarious and very clever ad campaign. But I will say…

NNAMDIYou can find a link on our website, kojoshow.org. Go ahead.

WEISSRight. So a major challenge for states and for the federal government is insuring that the young and the healthy people get into the marketplace. And this is in part because if you get those young and healthy people in then the risk, you know, the risk pool is better for everyone and you get a balanced approach, as opposed to just getting the sick people in the door. And so states were really focused on insuring that those healthy people, especially the young folks who think that they are never going to need health coverage, will get in.

WEISSAnd states did some really interesting and creative things last year that are worth mentioning and maybe replicated this year. The first is, you know, a number of states sponsored these social media campaigns. And they gave away concert tickets. Washington partnered with Death Cab for Cutie, which is an alternative band. And they made -- they put on a major concert.

WEISSKentucky apparently advertised with Hulu's streaming service and actually advertised on the "Kardashians" to try to sort of get young people interested. And there was just a lot of those sort of strategies to try to help interest young people and educate them about why this is important for them.

NNAMDIHere's Neal, in Silver Spring, Md. Neal, you're on the air. Go ahead, please.

NEALYes. Thanks for taking my call, Kojo. I am a self-employed person. And I've always been on my wife's plan. But this year my wife's employer is saying that because of the age base plans our cost has gone up quite a bit. And she will not cover -- or actually I will have to pay completely out of pocket for my coverage and, but what -- so I started to explore the options on the healthcareconnection.gov.

NEALBut my biggest concern is -- I can afford the coverage, but my biggest concern is that what happens if this -- whatever is going on in Supreme Court is against the Obamacare and then would I be left either here nor there and I won't be able to go back to my wife's coverage or not have to -- not be able to continue this coverage that Obamacare is providing.

NNAMDIKim Lankford and then Alice Weiss. Kim, you first.

LANKFORDWell, there's a lot of things that, you know, that you can be concerned about, but I think it's really a good idea to just go ahead and make your best decision for now. I mean, we'd probably have a heads-up before any major changes. And the other key thing is now that there's not -- you can't be excluded for preexisting conditions, you can really look at this as a year-by-year decision. And so really it's a good idea to go to your marketplace and take a look at what the costs would be. And see what the costs would be with a subsidy and without a subsidy.

LANKFORDIf anything changed in the future you could always switch to maybe a bronze policy that might cost less. But really it really is a year-by-year decision now. And that's something that people really need to keep in mind, that -- especially who had medical conditions in the past -- are not used to being able to shop for insurance from year to year. They would be in the policy, they'd be stuck. And then they couldn't get a new policy after they developed the conditions that made them need it more. So just take a look at it this year and make the decision based on this year's finances.

LANKFORDWell, as for your Supreme Court and maybe politically concerns Neal, Alice, part of the red wave in the mid-term elections may have been the mantra, repeal Obamacare. But a new Gallop poll shows that 7 in 10 Americans who bought health insurance through government exchanges are happy with that coverage. How would you assess the first year?

WEISSWell, it seems that consumers have had a positive experience. I mean, you know, every individual's experience is going to be different, but, you know, the Gallop poll suggests that there's a strong support for coverage. Secretary Burwell announced that something like 7.1 million out of the 8 million who enrolled in exchange coverage ended up staying with their enrollment by the end of the year. Some people dropped off because they couldn't pay premiums. Some people dropped off because they were actually ineligible.5

WEISSBut that's pretty -- that's a pretty high retention rate of the year. And I think people are -- seem to be enjoying and investing in the coverage. You know, there have been some issues that are important to watch. You know, there were some issues with concerns about narrow networks, that plans were sort of carving up who they were going to allow you to see in terms of providers and hospitals that were in the network for the plan.

NNAMDIAdequacy of coverage.

WEISSAdequacy of coverage. That was a big issue. Another big issue that we saw was concerns about the tiering of prescription drug copayments. And so for example if you're someone with a chronic condition like cancer or HIV-AIDS and you need access to these more expensive drugs on an ongoing basis, some analyses have shown that in these exchange coverage plans you're likely to pay a significant amount more.

WEISSSomething like as much as 38 percent more than you would in a typical employer-sponsored insurance plan. And that's something that I think, you know, regulators are going to need to be keeping an eye on.

NNAMDIWe got an email from Cee, who writes, "The D.C. exchange has been anything but a smooth ride. We signed up last year after spending many days on the phone. The website never worked. After the birth of our child, it took them five months to add her to our policy. Apparently a spreadsheet needed to be printed out and then typed back into the computer.

NNAMDI"Now, the joy has started anew. The website is still awful and full of error messages. The very nice Health Link staff never calls back. And now we're told that there is some sort of data corruption issue that is preventing us from changing our policy this week. I am very grateful and supportive of the Affordable Care Act, but it is so frustrating that we spent obscene amounts of taxpayer funds for a malfunctioning system."

NNAMDII should mention that D.C. Health Link wanted to join us today, but were unable to provide a guest. Alice, Jenna, can you help these -- this person and respond to some of these issues on the D.C. website?

JOHNSONWell, I'm more familiar with the Maryland website.

NNAMDII thought so.

JOHNSONBut a lot of the concerns that I'm hearing I've been hearing for past year in Maryland. You know, people who accidentally got enrolled in two plans, who are trying to get a child added, have had a life change. And sadly the only advice I have right here -- and maybe someone else will have some better advice -- is document every conversation you have and keep calling. There are a few people in Maryland that I've kind of followed along as they've dealt with this. And it's very frustrating and it takes a very long time. But for the ones that have finally gotten through it, they were very joyful when they did.

NNAMDIWell, patience is the word here, Cee, I guess.

WEISSYeah, the only other thing I would offer is that I think, you know, it's really important to take advantage of resources that are available to you. So exactly -- as was just expressed, you know, it's really good to document all of the interactions, but also there are assistance organizations that may be able to advocate for you and pick up the ball for you and help you with the process. And I would definitely take advantage of those.

WEISSBut the sort of experience that you're having with D.C. Health Link is not necessarily atypical, in the sense that is a ton of -- there's a ton systemic complexity in standing these systems up. And then you think about the fact that it had to happen in, you know, in 16 states, including D.C. And then with the federally facilitated marketplace, which is a huge enterprise technically.

WEISSYou know, I had heard from someone who works on these issues that it took, you know, the airlines something like 10 years to create a system to just be able to help you assign your seat electronically. But if you think about all of the multiple transactions that need to happen in terms of data exchange with these systems, and the fact that they had to stand up in relatively quickly -- a quick amount of time, I would just say, you know, please understand that the state folks are really trying, the technical folks are trying. And be patient and be persistent.

NNAMDIKim, I want to get back to an issue that you raised earlier and that is the issue of chronic conditions. I thought one of the hallmarks of Obamacare was minimum coverage and not weeding out people based on preexisting or chronic conditions.

LANKFORDThat's correct. And so that's a key thing that a lot of people who for years and years in the past, before the ACA was passed, had to stick with their policies because they were going to be rejected if they switched to another insurer -- no longer need to worry about that. So it's also -- you know, I've talked with a lot of readers, you know, readers with diabetes, readers with cancer, lots of conditions who may have not been used to being able to shop around for coverage. They were stuck with what they had.

LANKFORDSo they also need a reminder that, you know, this open enrollment is for everyone. And they can look around and they can look at the policy that has the best coverage for them. And a key thing when you do have conditions though, is to look at what the policy covers. Make sure that your doctors and your specialists are included in the network. And that was one of the biggest surprises people had when they went to use their policies last year, was some of them, you know, the insurers that they'd been with for years, may have offered new versions of their policies with much smaller networks that didn't include their doctors.

LANKFORDAnd so when they went to use their doctors, either they had a much higher copay, or if they weren't an HMO, they may not have had any coverage at all outside of the network, except for emergencies. So make sure the doctors are covered. And also, prescription drugs. There can be a huge range of coverage. So don't just make sure that if you have a health condition and expensive drugs -- don't just make sure it's on the health plan formulary, which is the list of drugs that are covered, but find out how it's covered.

LANKFORDIs there a $10 or $20 copay? Or, which is more of the case for some of these expensive brand-name drugs, are they charging you 30 to 50 percent of the total cost, which could still be hundreds of dollars a month if you have an expensive drug. So look at premiums, but also look at networks and how your drugs and the types of care that you need are covered, what your overall expenses are going to be.

NNAMDIAlice, how are these plans regulated now and what sort of oversight is there and what might be needed going forward?

WEISSWell, the plans are regulated for the state-based exchanges at the state level, and for the federally facilitated marketplace they're regulated at the federal and at the state level. There are a variety of requirements that were created under the ACA that create sort of a minimum threshold of protections, including the protections we've been talking about, preexisting condition exclusions and others. And states are supposed to be enforcing those.

WEISSAnd if they don't substantially enforce them the federal government has the authority to come in and make sure that they're doing better. The secretary has issued -- the secretary of HHS has issued a number of guidances to help people understand what the minimum coverage should be and address a variety of issues that have come up. And there are still probably some opportunities for both the states and the federal government to sort of make sure that they're bringing their regulatory oversight up to the level that's needed based on what we're seeing in the marketplace.

NNAMDIJenna, this got attention in Maryland. One of their providers, United Health Care, is offering plans that do not cover care in the Johns Hopkins Health system. That's a big one in the state. Which leads to the question, how important is it for people to understand which health care networks they're able to use?

JOHNSONIt's very important. One of the big problems last year with the site being so difficult to use is that once people finally got in a lot of times they said, just give us whatever. And something like 94 percent of people ended up in plans offered by Care First, which, you know, maybe for all 94 percent of them that's exactly what they wanted. But from a lot of people I talked to they weren't looking at the details. What's covered, what's not covered, what's it going to cost them out of pocket, what are the perks?

JOHNSONYou know, what best fits their lifestyle? And so there's a hope that this year there will be much more of a focus on that. Maryland when through several rounds of negotiating rates with the four providers that are are on the exchange. United is a newcomer this year. Two of the others that had been o there, Evergreen, which is a health co-op and Kaiser, have brought their rates down. And those are now more affordable than the Care First plans. So it'll be interesting to see what people opt for this year.

NNAMDIOnto the Ramone -- oh, Ramone is no longer on the line. In this case we will go to Robin. Robin, in Frederick, Md. Robin, your turn.

ROBINHi. Thank you for having me on the show. I just have a comment. I listen to a lot about Affordable Care and having heard the advertisement about being lucky a while ago, the cute advertisement, but it -- and the word affordable, it just made me think. I have a son who's a 30-year-old self-employed. And he used to be able to get what they call catastrophic or major medical and just pay out of pocket for when he went, you know, to a primary care.

ROBINNow that option is not available anymore. It was a low deductible because it was catastrophic. So now his only option is to pay a high deductible and higher premiums per month. So I think the affordable part is only affordable if you have a drastic need. But if you're making, you know, $30,000 to $45,000 a year it's a big part of your income that still has to go towards it. So that's my comment.

NNAMDIKim Lankford?

LANKFORDWell, a key thing, if you are in that income range, really find out what the after subsidy cost is going to be. Because if you earn less than $46,680 and are single -- and for a family of four it's $95,400 -- those are the people who qualify for a subsidy. And all of the exchanges have calculators that show you what the post-subsidy cost would be. So if you're looking at some of these average premiums, you're actually not going to pay quite that much.

LANKFORDAnd if you're less than 250 percent of the poverty level -- so that was -- 400 percent is maximum for the subsidy, but 250 percent, you also get help with some of those cost-sharing things, the co-insurance and the deductibles and all of that. So it's really important to go on the website. Also Kaiser Family Foundation, kff.org, has a really good calculator, just really fast and easy that you can type in your age, you can type in where you live and you can type in your income. It'll just really give you a quick, quick estimate of whether you'll qualify for a subsidy or not. But also, if you do have a high deductible policy, which so many more people do these days, it's important to think about making sure that that's an HSA eligible policy.

LANKFORDA Health Savings Account lets you put in pre-taxed money and then you can use that tax free for medical expenses in any year. And, you know, if you don't have a lot of money, it might be tough to contribute much. But even contributing a little bit can help you kind of lower your taxable income, stretch that money, can help you maybe even lower the income that would be used to determine whether you qualify for a subsidy.

LANKFORDSo just find out if the policy -- if it has at least a $1,300 deductible for an individual or $2,600 deductible for family, ask the insurer if it's HSA eligible and see if you can at least make the most of that. That can stretch your money a little bit further.

NNAMDIArlene, thank you for your call. We have to take another short break. If you have called, stay on the line, we'll try to get to your calls. The lines appear all filled up. So if you have a question or comment, shoot us an email to kojo@wamu.org or a tweet @kojoshow or go to our website, kojoshow.org and join the conversation there. I'm Kojo Nnamdi.

NNAMDIWelcome back. We're talking about the Affordable Care Act and health care exchanges in this period of open enrollment. We have Kimberly Lankford, contributing editor with Kiplinger's Personal Finance. Alice Weiss is the program director for the National Academy of State Health Policy, NASHP, which is an organization of state health policymakers. And Jenna Johnson is a reporter with the Washington Post.

NNAMDIJenna, Maryland's botched health care exchange rollout last year was embarrassing for Maryland. Do we know whether there were political repercussions in a blue state that unexpectedly elected a Republican governor two weeks ago?

JOHNSONYou have to think that this was one of the things that helped Larry Hogan win in Maryland. As I was reporting over this -- on this over the last few months, there was a lot of confusion in Maryland about what exactly went wrong with the exchange, who exactly was at fault, exactly how much it cost. I think a lot of people just thought, you know what, the federal exchange was screwed up, other states were screwed. It's all very confusing. I don't know who to blame for this.

JOHNSONWe even did a poll in the spring and asked people who's responsible for these problems. And we gave them a bunch of options like Martin O'Malley, the governor and the lieutenant governor, Anthony Brown, who's in charge of health care reform. And, you know, or they could blame it on state employees or other and they could offer up a name. And we had more people offer up Obama's name as being responsible than pick Anthony Brown, who has been criticized for not doing enough to avoid this.

JOHNSONYou know, when I talked to voters, the biggest frustration that I hear is not just that things went so wrong, but that there just wasn't much transparency about what happened. And that there seem to not be an appreciation for their taxpayer dollars and how those were being spent and what the state was doing to hold people responsible.

NNAMDIAlice, 22 states declined to expand Medicaid using federal dollars. What does that mean for Obamacare overall? What kind of coverage gap does that leave?

WEISSWell, that's a really important issue. Kaiser Family Foundation put out estimates of how many people are affected by this coverage gap and they estimate about four million low income adults fall into the coverage gap. And most of them live in larger states like Texas, Florida, North Carolina and Georgia. Another recent report found that the median income of those affected is really very low.

WEISSSo about 65 percent of the federal poverty level or less than $10,000 as a monthly income for three. And so, you know, this is a real issue for many, many people. And the other thing that's really tragic is that the majority of people who live in these states -- the people who are disproportionately affected are African Americans, Latinos, people who are less likely to have a college education.

WEISSSo really all of the people who you think are more likely to want or need assistance in terms of, you know, if you're thinking about disproportionate health disparities and things like that. So you really want to figure out how to solve this problem. But many of the people living in these states -- if you're under 100 percent of the federal poverty level or $11,000, a little over $11,000 a year for an individual, then you're basically going to be without coverage.

NNAMDIOn to Joseph in New York City. Joseph, you're on the air, go ahead please.

JOSEPHYes. I have a success story. I am an artist in New York and I was accepted to the Torpedo Factory last September to do a residency there, but found out I had a brain tumor in my head, the size of a fist, like, two months before the residency. I -- Obamacare covered everything and I was able to do the operation and get residency the next month. So a good feeling for the success that this has...

NNAMDIAnd you've -- and you encountered no obstacles along the way, Joseph?

JOSEPHNothing at all. I was -- I was really, really surprised. And, you know, you're going through so much other stress, you don't need it through the coverage at all. So, just a success story to share with everybody.

NNAMDIThank you very much for your call. Speaking of success stories, Alice, your organization doesn't weigh in on political wrangling. But we did see in the midterm elections that red wave across the country, heard a lot of talk about repealing Obamacare and in the news right now are videos of controversial remarks by one of Obamacare's architects, Jonathan Gruber, which is helping to fuel opponents.

NNAMDIAs I said, you don't weigh in on political issues, so to speak. But you do note that there may be pressure on those opposed to the ACA to walk that line back a little. Can you explain?

WEISSWell, I think that this was -- this was just recently documented in the New York Times talking about how, you know -- there are so many people that are now invested in the ACA and ensuring that it's implemented and that it stays in effect, not just the people who need coverage, but now all these insurance companies who are selling coverage to people in Medicaid and in the private exchanges.

WEISSAnd so, really, you know, there's a new constituency, a very powerful corporate constituency that may -- may end up exerting some influence on the new leadership in Congress and on new governors to try to see what opportunities there are for sustaining the ACA and even, in some cases, maybe even expanding Medicaid in states that have previously been opposed.

NNAMDIBack to specifics. Here's Alex in Arlington, VA. Alex, you're on the air, go ahead please.

ALEXHi there, Kojo. First of all, let me thank you very much for your program. I feel after each show I'm a lot smarter than I was before.

NNAMDILikewise.

ALEXYeah.

NNAMDIGo ahead.

ALEXThank you, sir. I'm going to be 65 in February and I'm currently on a Care First Blue Cross ACA policy. What do I do now? What do I do when I turn 65 in terms of Medicare?

NNAMDIKim Lankford?

LANKFORDAnd that is a great question, because signing up for Medicare in the middle of the year can always be tricky, but so many people go through that every year. Go to Medicare.gov and it gives you a lot of great information about the steps that you'd need to take to sign up for Medicare. Make sure that you that within the timeframe. You can start to do it a few months before you're age 65, but just make sure that everything kind of goes smoothly in that transition from your policy -- from your ACA policy to Medicare.

LANKFORDBut Medicare.gov has a lot of great information. Social Security -- Social Security Administration website or calling their number has a lot of great information, too, that really just walks you through step by step to make sure that you don't have any gaps in coverage. Also make sure that when you are signing up for Medicare that you think about what you're going to do to fill in some of those gaps, whether you're going to get a Medigap policy, a Medicare supplement policy that, you know, covers some of those -- some of those out of pocket expenses that Medicare doesn't cover.

LANKFORDAnd if you're going to get a part D prescription drug policy, to cover prescription drugs, which are not covered automatically under Medicare or if you want to get a Medicare advantage policy, which covers drugs and medical expenses through a private insurer. So start thinking about those options and then just a step by step logistics that'll really help walk you through.

NNAMDIAlex, thank you very much for your call. Good luck to you. Kim, I'd like to get into more specifics about plans and coverage. How do this year's plans compare to last year? What's changed? And how much of a price hike will people see?

LANKFORDYou know, it really varies a lot based on what you're looking at. I mean, some of the averages we're saying that, you know, there are increases about 5 to 7 percent on average. But it's interesting if you look especially in Maryland's -- Maryland and D.C. and Virginia, at the difference in the price ranges for the second to lowest silver plan, which is what they call the benchmark plan. That's what the subsidy is based on.

LANKFORDAnd that's kind of, you know, kind of an average plan versus the increases for the bronze plans. I mean, on average, the price increases for the second to lowest silver plan in the area are about , you know, 2 percent, 2.5 percent, a little bit more than that. But the average increases for the -- for the lowest cost bronze plan in the area tended to be much more than that. Not in Virginia but in D.C. and Maryland.

LANKFORDAnd so, it really -- it really makes sense to take a look at all of your options because if you stick to the plan that you have, some of the other plans may have come in a lot cheaper or your plan may have changed or some new insurers may have come in and offered new options. So the landscape is really different. And just looking at what your own price increase -- it may have -- you may have gotten a surprise and seen that your price may have, you know, increased more than some of those averages.

LANKFORDBut then, take a look at your other options, especially in your -- in that middle range that you're in, whether you're silver, bronze or gold. But also, you know, if you realize that you didn't have a lot of medical expenses, you want to lower your premiums, maybe look at some of the bronze policy that you have some of the higher medal levels. On the flip side, if you are going to have surgery this coming year and know you're going to have a lot of expenses, this may be the year to switch to a silver or to a gold plan.

LANKFORDPay a little extra money, but have a lower deductible. And then the year after that, you can switch back. So like I said before, it's something you can really make a year to year decision, looking at what the landscape's like exactly in that year, because it varies a lot.

NNAMDIAlice, we got an email from Jackie who says, "My question concerns portability of a plan. My daughter and her husband, late 40s, live in Maine and they will be moving sometime in the next year. They signed up under the Maine state exchange and move. How do they maintain their insurance? Do they need to go sign up in another state if they stay in the U.S.? If they were to go overseas, how will their insurance work?"

WEISSRight. So I think that -- one thing that they'll need to look at is they'll want to make sure they understand the terms of the plan they're signing up for and ensure that there's some provision that deals with if you move out of the geographic service area sort of what happens. I think, you know, moving into a new area may be a factor, which could help them qualify for a new coverage. If they lose their coverage mid-year, they may be eligible to apply outside of the open enrollment period.

WEISSBut it's something they should look at very carefully. I want to just follow-up on one point that Kim was making about the choice of different plans. It's important to underscore that, you know, people are only eligible for the federal assistance for the subsidies, the premium tax credit or the co-sharing subsidies, if they buy a plan at the silver level, the second lowest plan. So that's something to keep in mind as you're considering sort of what something's going to cost.

WEISSIt's not just the cost, you know, on the -- on the sticker price, it's sort of what it would be if you got your subsidy. And then the other thing that's important to note is that a lot of these cost increases, it seems, according to some analysis that was done by the New York Times, have occurred -- been highest in areas where there's less competition. So the ACA was intended to create more competition among insurers, bring more insurers into the marketplace.

WEISSAnd in some cases, especially in rural areas, that doesn't appear to be happening as much. And so, in those places where insurers have more of a market share and there are fewer competitors, it seems like, insurers are now charging for their coverage.

NNAMDIHere's Chris in Rockville, MD. Chris, you're on the air, go ahead please.

CHRISYeah. I'm a retired federal employee, so I have the federal insurance. Thank God I don't have to worry about this. I have some graduate study, but I don't think I could really make heads or tails out of all the different plans. I'm just curious when they were doing these plans, why didn't they go to Walton Francis, the expert who does the Washington checkbook guide to help plan for federal employees?

NNAMDIAnd a frequent guest on this broadcast, but go ahead.

CHRISOh, okay. Because, I mean, what's incredible that he does is that he'll say, look, don't just look at the premium, high option or low option, and then he sets up this book you can get every year that says, okay, are you a single person? Are you a couple? Family of four? Larger family? Retired? Using HMOs? Using, you know, the main plans? And do you expect low, average, or high...

NNAMDISo you want to know why -- why -- who did not do the same thing?

ALEXAnd I'm just curious, yeah, because I don't think the federal government or the states ever went to use this guy and he's incredibly good?

NNAMDIWhy didn't you consult with this guy, Alice Weiss?

WEISSWell, I was just going to say, you know, that the states and the federal government have provided for some degree of assistance that's comparable to this, right? They have navigators, they have different types of in-person assistors. Brokers and agents are supposed to be able to walk you through these options. The caller before was talking about Medicare. There are state health insurance program, which are Medicare-based assistors to help you understand the variety of coverage options.

WEISSAnd many states also created these plan comparison charts that help you understand it. But you do need to be very careful and understand the full scope of your costs and your needs in signing up.

NNAMDIAnd the bottom line, Chris, is that it is my understanding that whether you buy through the exchanges or not, it should be easier this year. But that's all the time we have. Kimberly Lankford is a contributing editor with Kiplinger's Personal Finance. Kim, thank you for joining us.

LANKFORDOh, thanks for having me.

NNAMDIJenna Johnson is a reporter with the Washington Post. Jenna, thank you.

JOHNSONThank you.

NNAMDIAnd Alice Weiss is the program director at the National Academy for State Health Policy, NASHP, which is an independent organization of state health policymakers. Alice, thank you for joining us.

WEISSThank you, Kojo.

NNAMDIThank you all for listening. I'm Kojo Nnamdi.

On this last episode, we look back on 23 years of joyous, difficult and always informative conversation.

Kojo talks with author Briana Thomas about her book “Black Broadway In Washington D.C.,” and the District’s rich Black history.

Poet, essayist and editor Kevin Young is the second director of the Smithsonian's National Museum of African American History and Culture. He joins Kojo to talk about his vision for the museum and how it can help us make sense of this moment in history.

Ms. Woodruff joins us to talk about her successful career in broadcasting, how the field of journalism has changed over the decades and why she chose to make D.C. home.